Car Talk # 47 (On Autonomy)

Hi friends

I finally migrated to Substack! This has been a backburner project but I was surprised at how easy it was to export all content and subscribers out of the older platform to here.

What changes for you? Not a thing. CarTalk will remain free, possibly insightful, certainly irreverent.

What changes for me? I might be able to compose a newsletter with one hand while pushing a stroller with the other. Don’t worry about potholes - I only traverse streets I’ve mapped a thousand times before, like Waymo (heyooooo). CarTalk’s past issues are also much easier to share now - the URL simply is cartalk.substack.com.

This issue has no weekly updates. It is a reflection on where autonomy is headed. These are just my opinions. I hope some resonate.

Buckle up!

Autonomy: Winner-Take-All

This has been a busy couple of weeks for autonomous driving news. I was glad I don't have to report on this space for a living. Those who do were feeling the pain!

What was going on? A lot, as it turns out. But before we get into the meat of it all, let's set the table real quick.

Long time CarTalk readers don’t need to be convinced that the market for autonomous driving will be substantial (once we get it to work out of the box, that is). A year ago, McKinsey was predicting that 2/3rd of all passenger travel will be autonomous by 2040. Today, some of that optimism might be a bit tempered. Even so, the world population is expected to be 8.5 billion by 2030, 9.1 billion by 2040. Trillions of trips will be taken by this mass of humanity. Autonomous travel will account for a massive share of moving mankind.

Bottom line is that this is a space rife to be monetized. Again, no real “aha” moment if you’ve been paying attention.

Okay, so what has been going on that’s causing automotive reporters to burn the midnight oil? A couple of noteworthy things:

Argo.ai (backed by Ford and VW) has taken on Lyft as an investor and will allow Lyft’s platform to offer self-driven rides in Miami and Austin by end of this year. Lyft will own 2.5% of Argo (last valued at $12.4B). Is Lyft suffering from FOMO? I do think so. Last year, they divested their own AV division to Toyota for $550M. Will the rides be human-free? Nah. It’ll still have two safety drivers in the driver and passenger seat. Still - I consider it good news that the players are consolidating in the autonomous space. Link

Toyota acquires CarMera (a play on camera? chimera?). CarMera develops high-definition maps that are needed (some say) to unlock autonomous driving:

The teams will tap into CARMERA's ability to successfully update HD maps from crowdsourced, camera-based inputs―a significantly cheaper and faster approach than traditional methods. This will strengthen AMP's ability to serve a comprehensive set of road classes and features, reflecting changes in lane markings, traffic signals, signs and more in near real-time, and support its future multi-regional commercial launch.

Keywords to latch onto here: crowd-sourced (obviates the need to hire drivers to drive in circles around SF or NYC to map streets) and camera-based inputs (no fancy LIDAR, radars, sensing suites needed). Cheap as well as fast!

If you’re in the camp that firmly believes that HD Maps are the way to full autonomy, you’ll appreciate why this deal might be big for an OEM like Toyota.

Intel’s Mobileye starting to test AVs in New York City. Is this a big deal? I think so. It displays Mobileye’s confidence in tackling an area other AV players have shied away from

While other states have become hot beds for AV testing, New York has been a bit of a ghost town. Part of the reason could be the state’s strict rules, which include mandating that safety drivers keep their hands on the wheel at all times and requiring state police escort at all times to be paid for by the testing company.

I did not know that last part! If Mobileye is willing to pay their own safety drivers as well as cops, they better have something to show for it soon. Mobileye is interesting because they’re aiming to be opportunistically a B2B or a B2C company, depending on market context. This interview with a Mobileye VP was exceptionally telling:

Look at our Moovit acquisition. That brought the capability and back-end intelligence for us to be able to offer a direct-to-consumer mobility service. In other markets, maybe we sell the automated vehicle capability to a manufacturer and they put it in their car. We’re not putting all our eggs in one basket.

Magna, an automotive tier-1 company (NYSE: MGA) acquired another tier-1 company Veoneer (NYSE: VNE) at a 57% premium to its last closing price in a cash deal valued at ~$4B. That is some serious cash. What did Magna get in return? They got a company that builds ADAS systems like front-facing cameras, thermal systems, radars and so on.

ADAS is the pit stop you need to make on the road to full autonomy, the conventional thinking goes. Waymo, Zoox etc. disagree, of course. Magna wants to own that pit stop and are happy to pay tres comas for it.

I covered this already in a prior CarTalk issue but Aurora is going public via a SPAC IPO, while Waymo raised $2.5B in their latest round.

There are a number of other updates in the same vein, but I’ll stop there.

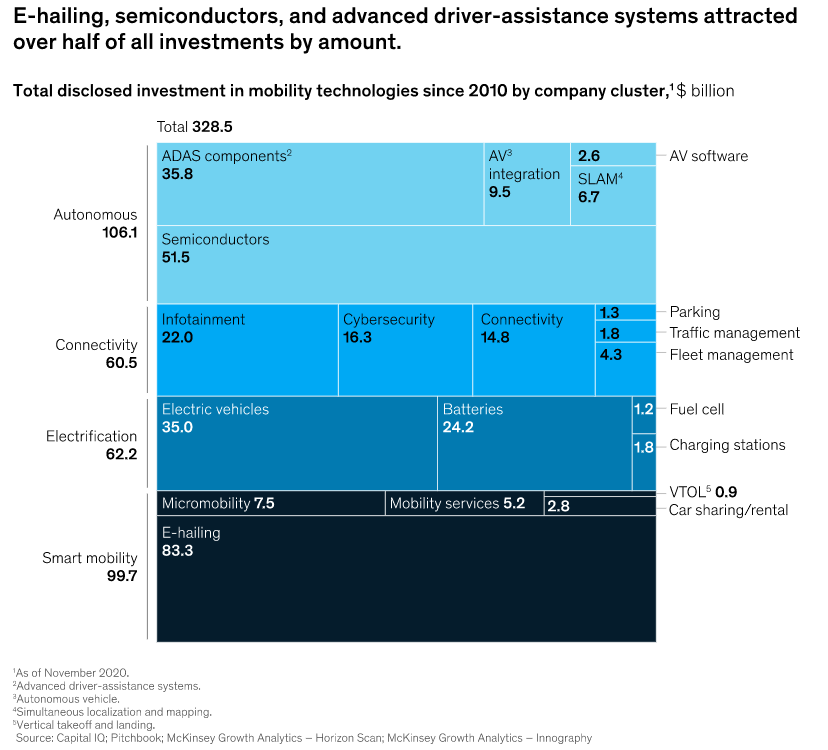

Recall again what’s at play behind all these movements: moving 8.5-9 billion people autonomously over the course of the next 10-20 years. No wonder, then, that so much money is being spent on Autonomy relative to all other new mobility paradigms (Connectivity, Electrification, Shared mobility). For a long time, this used to be my gut feel. However recently, McKinsey quantified it for us:

As of November 2020, one in every three investment dollars in the new mobility space went towards Autonomy ($106M out of ~$330M total). This money is funding essentially the backbone of the transportation network of the future. It begs the question - what exactly is the money going towards? How do we know it is even the right place to be investing? Again, McKinsey to the rescue (hey, that’s a brand new sentence!):

Cool visual, right? Zeroing in on the top row for a second, there are many ‘clusters’ within Autonomy that are consuming investment dollars. For Autonomy in various contexts such as robo-taxis / long-haul trucking, will all these technology clusters need to be production-ready? That is to say, do we really need Radar + Camera + HD Maps + SLAM + AI Image Recognition +… to work before we get Autonomy?

No. I don’t believe so. And many in the self-driving space don’t either. There are conventionally two agreed upon ways to unlock Autonomy:

Vision-only stacks - only cameras are the “eyes” of the car. No other sensors are needed. Adhering to this philosophy are Tesla, Mobileye etc.

Full sensor-suite stack - requiring cameras + radars + LIDARs + thermal cameras, all integrating to inform steering and motion. Members of this camp are Waymo, Zoox, and basically every other AV player.

Of course, each Autonomy aspirant hopes their tech stack wins. In the vision-only camp, Tesla has always been all-in on cameras. No love for expensive sensors like LIDARs. Recently, we gave up on radars too. Tesla’s bet is that all that is needed to unlock full autonomy are cameras + high performance compute + advanced software.

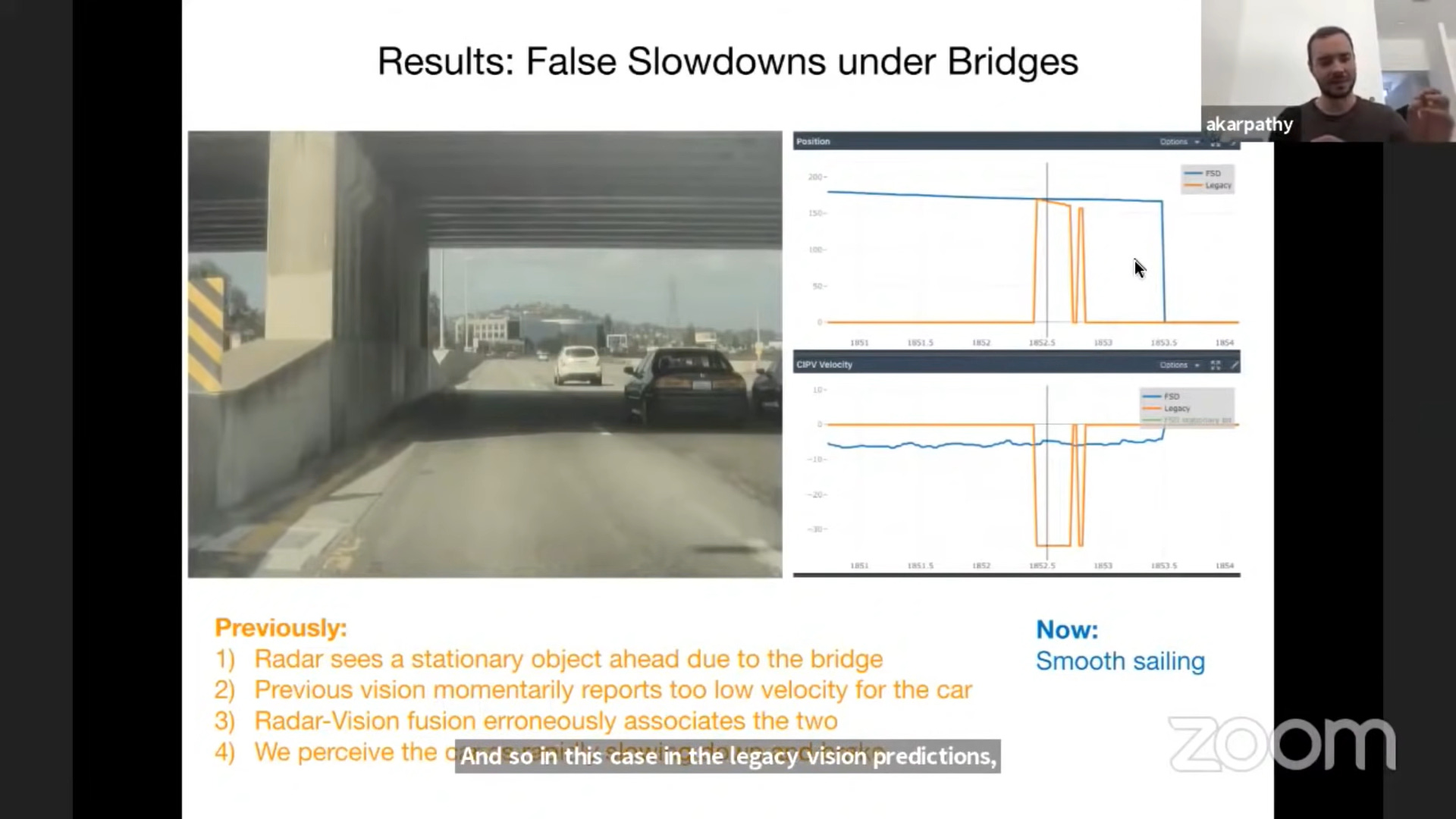

A brief detour: You might think - are just cameras sufficient? How can radar and vision disagree? An obstacle is an obstacle is an obstacle, right? I learnt from this cool talk by Tesla’s chief Autopilot engineer that radar and cameras often didn’t…see eye to eye (pardon the dad joke):

Tesla figured the radar was reading the static bridge as a stationary obstacle (oscillating orange line) and would brake sometimes when a car passed under a bridge, while the camera kept going because the neural net knew what a bridge is (steady blue line). Tesla learnt that the radar was introducing noise and decided to remove it, thereby improving its tech stack continually. Brief detour ends.

In the Full sensor-suite camp, Waymo and others are improving their tech stack continually also. Waymo, for instance, starting making its own LIDAR as a way to strengthen its tech stack. Waymo is also big on simulating real-world collisions in software - they are best known to simulate freak scenarios in computer code and then update their fleet with lessons learnt to improve safety.

Simulation is a critical piece of the puzzle for autonomous vehicles. These programs allow Waymo’s engineers to test — at scale — common driving scenarios and safety-critical edge cases, the learnings from which it then feeds into its real-world fleet.

Like Waymo, every other AV company is continually refining its tech stack, betting that their tech stack wins. This is super cash intensive, but as these companies have shown, raising cash is not an issue. What is of prime concern is getting Autonomy right and planting the winner’s flag.

Winning, in my opinion, is really important in this space. Generally, the second-to-market company has to be satisfied with a smaller share of the pie. In the case of Autonomy, however, the second-to-market company might not get any pie at all.

A bit dramatic? I don’t believe so.

It is my personal belief that autonomous driving is a winner-take-all technology. Let’s align on what winning even means in autonomous driving. If you ask me, the metrics to judge AVs will be:

Safety of the tech stack - disengagements, damage to the vehicle in collision, death of riders, etc.

….that’s literally it. Safety won’t be graded on a curve, it will be a pass/fail: either a tech stack is safe, or unsafe.

The safest tech stacks are the ones all vehicle manufacturers (vehicle = car, bus, truck, ship) will gravitate towards. No vehicle maker in their right mind will partner with an autonomous company that is right only 99% of the time when there is another one in the market that is right 99.999% of the time (geo-fenced applications aside!). OEMs have too much to lose in that final 1%.

What if there’s a tie between two AV stacks? e.g. both are seemingly the best ones? In that scenario, the tie-breakers will be:

Geographic range of operation of the tech stack - can the stack work anywhere in the world? Does it work only on paved roads but not off-road? Does it require certain pre-mapped routes, or can it freestyle?

Cost of the tech stack - does it need expensive sensors, computers? Or can cheaper cameras and custom computers do the trick?

(If you wanted to tell me to reverse the order of 2 and 3, I wouldn’t put up a fight.)

In summary, winning in Autonomy means the best:

Safety. Non-negotiable.

Geographic range

Cost

Why do I consider Autonomy a winner-take-all product. By definition of winner-take-all:

A winner-takes-all market refers to an economic system where competition allows the best performers to rise to the top at the expense of the losers.

Any AV company that messes up Safety during their course of operation (e.g. everything is going well for them until the cameras on a car see something extraordinary - like a man dressed in a clown suit riding a unicycle - making the car go berserk and swerve into a tree), or is weak in their geographical range (e.g. an autonomous stack that works safely in Singapore but disengages often across the bridge in Kuala Lumpur) or cost (stack way too prohibitive to implement in every vehicle due to expensive sensors) will only drive its end customers (vehicle manufacturers) towards the best performer - unless the OEM is heavily invested in said AV company via a joint venture, or other corporate affiliations.

The best performers in autonomous driving will start to become aggregators, as defined by Ben Thompson of Stratechery. Ben defines aggregators as:

For aggregators, customer acquisition costs decrease over time; marginal customers are attracted to the platform by virtue of the increasing number of suppliers. This further means that aggregators enjoy winner-take-all effects: since the value of an aggregator to end users is continually increasing it is exceedingly difficult for competitors to take away users or win new ones.

I see that happening. Here’s a simplistic example - say autonomous company XYZ is slightly better than its competition when it comes to Safety. Its competitors ABC and KLM are good too but find a tree to hug every couple of months. When the time comes for vehicle manufacturers like Audi, Mercedes, Daimler to pick an autonomous tech stack for their next year model, they’ll gravitate towards XYZ (best safety, yo!). This benefits XYZ in multiple ways:

Safety: More end customers = more miles mapped by vehicles in various terrains = more labeled data that makes XYZ’s neural nets safer, strengthening XYZ’s lead over ABC and KLM.

Geographic reach: More road miles traveled by different OEM vehicles under various driving conditions + terrains + regions + countries = smarter neural nets, once again.

Cost (production): More end customers = larger production volumes = better economies of scale with XYZ’s own suppliers, lowering their production costs.

Cost (deployment): Marginal cost to XYZ of adding new customers = very low but non-zero since some non-recurring engineering will be required to deploy the tech stack into different manufacturers’ vehicles. Future updates will be nearly free - updating neural nets is like updating software.

Winning is what Argo, Zoox, Waymo, Cruise, Didi, Baidu, AutoX, etc. are all fighting for. They have staked their battlegrounds - Argo is a Pittsburgh city, Cruise and Zoox are SF-centric, Waymo has Phoenix covered. Here’s how I see this unfolding:

Step 1: Offering self-driven rides in their home turfs on pre-mapped routes

Step 2: Removing the safety drivers in the front seats (Waymo is here in Phoenix. This guy has so many videos of riding in driverless Waymos).

Step 3: Expanding scale of Step 1 (more vehicles, wider geographies, getting out of Beta modes)

Step 4: Expanding to a new city, starting at step 1

Do this a couple times without any serious issues/injuries, and voila, you’ve won Autonomy. Easier said than done, however. There’s going to be a lot of failure along the way before a victor emerges. Just hear someone who tried it and gave up:

And someone who will (thankfully) keep at it because the stakes are so high:

Even Mobileye gets it. Again, from their VP:

At the end of the day, the big prize is consumer automated vehicles. Because you think about how many passenger vehicles are sold on an annual basis to private consumers, versus the number of taxis purchased every year.

We’re making choices about our sensors and algorithms to make sure that this is not just a geo-fenced robotaxi service in dense urban environments. This is a capability that will allow you to own a car that can take you anywhere you want to drive.

Perhaps soon, perhaps in a decade, a winner will emerge. It is in preparation for that day that investors are pumping cash in the autonomous space, throwing every technology at the wall, yearning to be first to market. Winner takes all, remember.

What becomes then of #2, which may have been only a few months behind? The words of Ernest Hemingway come to mind:

How did you go bankrupt?

Two ways. Gradually, then suddenly.

That’s all from me folks. Have a great week.

If you liked reading this issue, please forward it to the last friend that sent you a funny gif. Cheers!