CarTalk # 51 (On Gogoro)

But really - more thoughts on the business of battery swapping

Hi friends

It is raining here in my neck of the woods as I compose this issue! Rain in NorCal is a bi-annual occurrence so I really should be playing outside. However, I’m gripped by the topic at hand and will contend with the pitter-patter on my window.

Welcome to new subscribers! I write about new mobility (electric, autonomous, shared, connected) every week or so. This issue side-steps automobiles entirely and goes straight to the world of two-wheelers. Weird for a newsletter called CarTalk, right? Not really! CarTalk is a newsletter on new ways of moving and two-wheelers move far more people than cars in certain parts of the world.

Buckle Up!

I was going to write an issue dissecting Rivian’s IPO and the S-1 they dropped a while ago. Long time CarTalk readers know I like their work, but their valuation is certainly jaw dropping ($80B, last I checked). As I started penning one, I talked myself out of it. Folks who do this sort of a thing for a living already have the high-level scoop here (TechCrunch) and here (G2 Venture Partners) already, so I’ll urge you to read their takes instead.

Instead, I want to summarize my thoughts on another S-1 that has been sitting on my desk - Gogoro. Gogoro, on the surface, is a Taiwanese electric 2-wheeler manufacturer with swappable battery packs which serve as the beating heart of their business, their competitive differentiator, as well as their biggest marketing tool / calling card. Gogoro has done really well in Taiwan already. Up next are China and India - major markets for two-wheelers!

Gogoro has written the playbook on how to run electric 2-wheeler businesses - so much so that if you’re a new e-bike company pitching to investors, you have to be ready to address “how is this similar/different from the Gogoro model”.

Why am I so curious about Gogoro? One reason: Swappable Batteries. Also helps that they are focusing on entering the Indian market. Color me interested!

The Basics:

Below is a quick visual of Gogoro’s 2-wheeler offering. The scooters are neat, elegant; the battery packs resemble a roll of paper towels that you can grab from Gogoro’s charging kiosks:

Gogoro would be interesting enough to me as a company if this is all they did. Turns out, they do much more. Gogoro’s business lines, as gleaned from their S-1, are:

Electric 2-wheelers, obviously

Battery swapping network

E-bike powertrain components to sell other 2-wheeler companies (Interesting!)

Services

Lots going on for a company valued merely at $2.35B and eyeing the world’s biggest 2-wheeler markets. Recall that Rivian, in contrast, is moving far fewer people and valued at $80B.

A snippet from Gogoro’s S-1:

Gogoro’s product offering is smart, swappable battery technology. Let’s get the “smart” out the way (a term used very loosely these days) - the batteries are connected to the cloud for geo-locationing and battery health diagnostics. Not only that, Gogoro’s phone app lets users check battery status, find charging locations, customize vehicle attributes (sound profiles, light effects, keyless auto-lock, Siri integration). As far as customer experience and customer obsession goes, Gogoro has thought their offering through!

Gogoro’s target market is urban riders in Taiwan, China, India. Very strategic, given these markets have the highest penetration for electric powertrain 2-wheelers:

By all accounts, Gogoro has done well thus far. They’ve sold 63 million 2-wheelers to date, as well as performed 200 million battery swaps (almost all in Taiwan). From their S-1:

The company has blitz-scaled in Taiwan, with 97% market share in the electric 2-wheeler market. The map of Taiwan, dotted with GoStations, tells a very compelling story. Some stats in the above slide are extraordinary:

>2000 locations in Taiwan

>400k subscribers

>800k batteries in use

>200 million swaps to date!

In summary - Gogoro has a good product on their hands. They’ve excelled at execution thus far in a small market and have an amazing runway ahead of them as they look to enter China and India.

The BaaS Business Model:

The Battery-as-a-Service (BaaS) business model allows a consumer to remove the cost of the expensive battery from the vehicle and pay for it with a pay-as-you-go model. In countries like China, India where upfront cost is paramount, BaaS models let you enjoy an EV for the low, low price of ICE. I wrote about this earlier and titled it “Rent your Range” (yes, still very pleased with the title!). The context was Nio’s launch of the ES6 EV sedan:

Here’s the deal - the Nio ES6 EV sedan costs ~$50k to buy outright. However, for customer who can’t pony up $50k, the company will let you buy the car without the battery for $40k and let you lease the battery pack for ~$140/month.

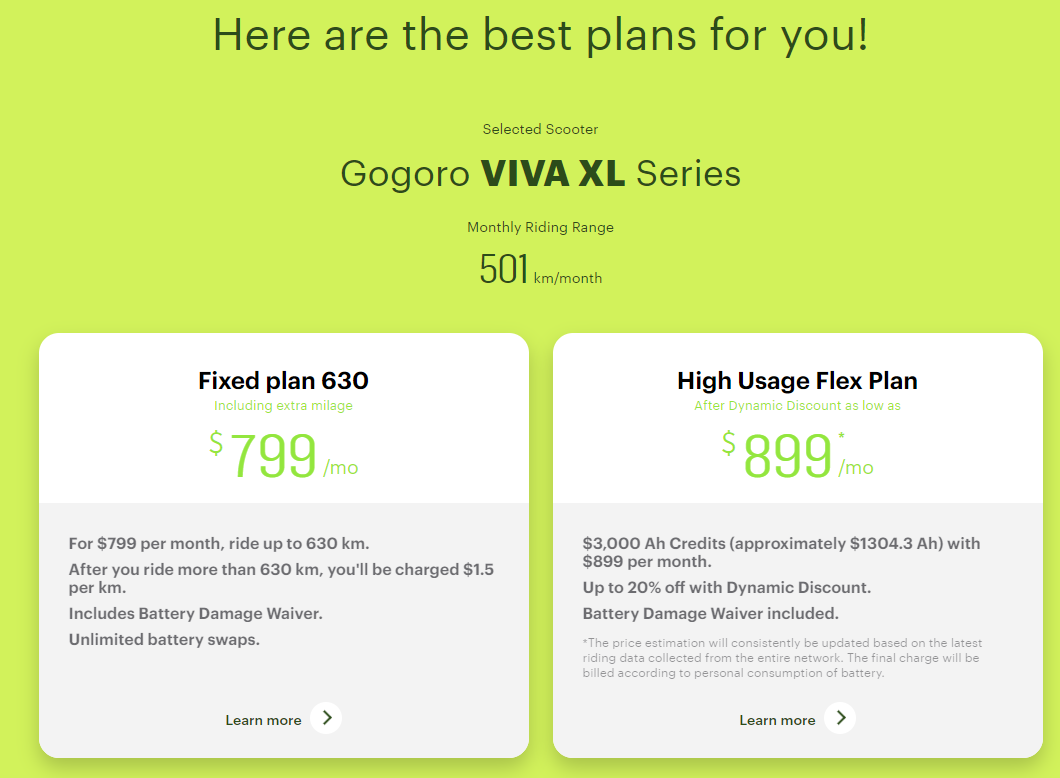

This is the same model Gogoro is going after - pay for the scooter now, pay for charged batteries on an ongoing basis. So you’d spend US $2500-2800 buying a scooter like the Gogoro Viva XL:

Once you have your scooter selected (and there are many, many models to choose from), Gogoro prompts you to pick one of many riding plans:

If you foresee your total monthly commute being within 630 kms, Gogoro will charge you NT$799/month (USD $29/month), or roughly a dollar per day. For longer distances, they’ll charge more.

To me, these prices feel a bit high. I wondered - what would operating a petrol scooter in Taiwan cost? A standard 125 cc scooter in Taiwan has a gas mileage of ~30 kilometers/liter. Petrol in Taiwan costs NT$31/liter. Thus to drive 630 kilometers per month, you’d spend USD $23/month. About 25% lower than Gogoro’s cheapest plan. Why would folks select electric scooters then?

A Taipei Times article from 2019 gave me the answer I was after - subsidies!

More than 82 percent of Gogoro Inc (睿能) scooter owners said that the government subsidies were the major reason they switched from a fuel-powered scooter, the white paper said.

Electric scooter buyers can receive as much as NT$30,000 in subsidies from central and local governments, making them more affordable. On average, the combined subsidies save buyers about 35 percent of the price of mainstream electric scooters, which retail for about NT$70,000.

Sounds like these subsidies have been reduced in recent times, but that’s not the scope of my article.

In summary, therein lies the beauty of BaaS - you can own an electric vehicle for the same upfront cost as a gas vehicle (yes, with the help of subsidies) and “rent your range” as you go! All enabled by the disruptive technology - battery swapping!

Layin’ It On Thick

Another advantage of a “rent your range” model is the recurring revenue it unlocks. Why profit off your customers just once, when you can keep doing it month over month? Every business out there wants to be a SaaS-lookalike these days and hypes up the subscription/recurring part of their operations (you can justify some really absurd valuations that way). Gogoro is no different:

Yes, they make money selling scooters and components to OEMs, but please look at their subscription revenue, won’t you?

As you go deeper into the S-1, you certainly notice how much Gogoro over-indexes on the subscription portion of their business (to the exclusion of scooter sales, electric powertrain sales, and other business lines highlighted earlier).

At the end of 10 years, 54% revenue comes from subscriptions and the rest from upfront sales. I didn’t see any mention of discount rates, inflation assumptions - it is simple arithmetic of taking a customer’s monthly revenue and multiplying it by 120. If Gogoro had adjusted for “real world” issues like inflation, the math might have come out different. Still, since they’re laying on the recurrence of their revenues thick, I’ll go along with it.

Math:

I love quantitative details in the S-1 deck, so was glad to see this view of BaaS revenue by cohort:

The 2019 cohort is expected to bring in the most revenue in recent years. 2019 was also the year when Taiwanese subsidies on e-scooters were at their peak. There have been more cuts to subsidies recently. Also, Covid put a kibosh on the 2020 and 2021 cohorts. All said - great chart! Very transparent.

Let’s anchor on the 2021E BaaS revenue - $104 million. Recall from an earlier exhibit above which said 839k batteries have been deployed by Gogoro and are in circulation.

If I had to triangulate “revenue earned per battery pack”, simple math would say $104M/839k = $124/pack/year. (Ideally, Gogoro would’ve deployed more than 839k packs by the time 2021 wraps up, but let’s keep this defensible).

The next obvious question for me - how profitable is this business model? Does $124/pack/year cover the costs of a pack, charging, maintenance? Or is it just an unprofitable hardware business once the SaaS giftwrap is removed?

Here’s what I’ve been able to figure out:

Each Gogoro pack is 1.74 kWh in capacity. Source (not sure how reliable).

Cost of a battery - $137/kWh at the pack level. Source (I consider them reliable).

Cost of Gogoro’s packs - 1.74 * 137 = $238/pack.

Cost/year to charge a 1.74 kWh pack (assuming 365 cycles/year and a high degree of utilization for each pack) = 1.74 kWh * 365 cycles * $0.128c/kWh (source) = $81/year.

Cost/year to maintain packs (cleaning etc.) = $5/year? Pure guess.

Assuming a 10-year lifetime:

Pack cost over its lifetime = $238 + $81*10 + $5*10 = $1098

Pack revenue over lifetime = $124*10 = $1240

Profit/pack over lifetime = $1240 - $1098 = $142

Yes this ignores time value of money, which would erode NPV of lifetime profits. It also assumes no extra cost for the packs being “smart” and cloud-connected - that can get pricey and would also would erode NPV of profits. Lastly, if the packs happen to be bigger and need more energy to full charge, you know what that does to the profits!

Is the BaaS business, then, a financially lucrative one? Rough math says…eh. At the same time, rough math also says it isn’t losing money at a unit-economics levels, so there’s that!

Houston, We’ve Been Duped:

Deep into Gogoro’s S-1 deck, I came across this slide:

They expect to grow subscribers rapidly due to expansions in India and China. However the middle slide for me was money:

What’s that shiny neon green label? For all the focus on battery swapping, Gogoro really expects to be making their money from selling enabling e-scooter hardware to other scooter OEMs. The darker green “Battery Swapping Subscription” label doesn’t grow nearly as fast as I would like - the sort of detail you only appreciate when you linger long enough on this slide. Otherwise, a casual breeze through the deck would lead you to continue believing that you’re investing in a SaaS-like company.

What exactly is Enabling Hardware? This slide explains:

Gogoro will sell the Swap-and-Go powertrain systems to a number of scooter OEMs to help them electrify their fleets quickly. This is akin to being a Tier-1 in the automotive space - the likes of Autoliv, Denso, Bosch, etc. And it makes sense - the R&D has been done, the more they deploy the more they crowd out any competitor. While its not exactly a winner-take-all market, Gogoro’s head start in the space and strategic partnerships have set them up for success.

Speaking of strategic partnerships, as the top half of the slide shows, they’ve locked down a number of high profile OEM partnerships already across India and China. The Yadea announcement in China was a big one. So was Hero in India. Is it that big of a deal, however? Partnerships come and partnership go! See GM and Nikola, recently. Will OEMs want to outsource the most critical technology in their scooters to a third-party? This is the question I’ve been grappling with on the automotive side and am still in the camp of denial/dismissal. In my view, the automotive OEM that controls their own powertrain wins. This is why Ford is announcing battery factories left and right, while GM is getting into multi-billion partnerships with LG Chem.

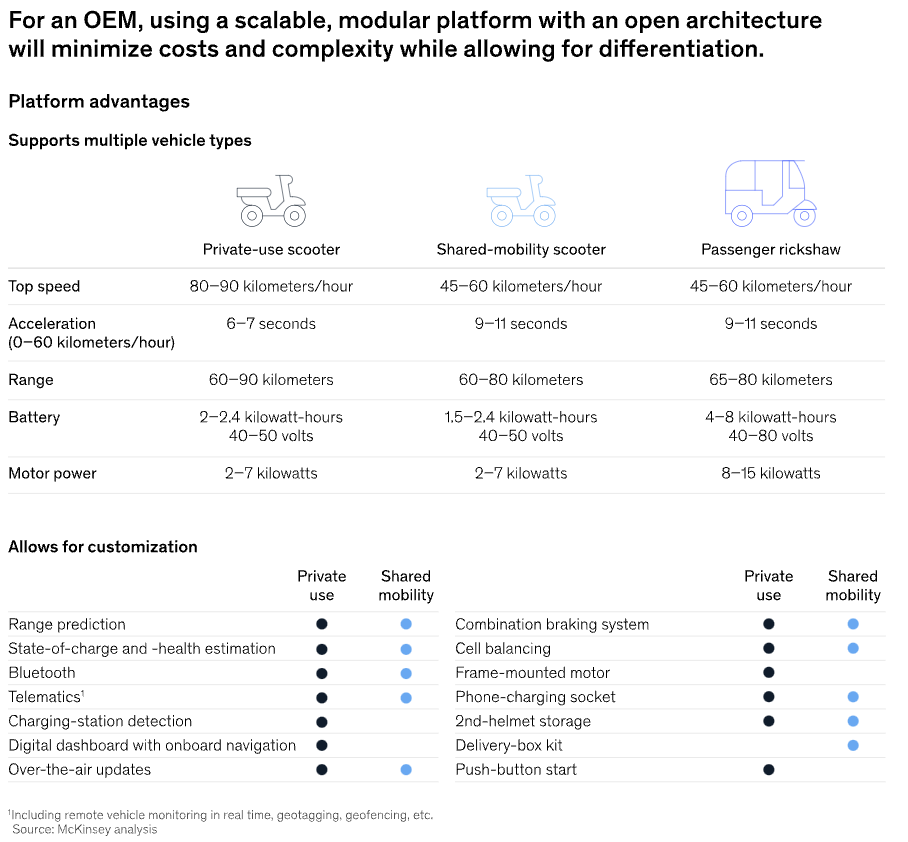

On the electric two-wheeler front however, there is a case to be made for OEMs to triangulate around a common platform/architecture, while finding other ways to differentiate themselves. In the McKinsey article titled “Global emergence of electrified small-format mobility”, the authors show how OEMs can adopt a common architecture to minimize costs and complexity, while finding ways to differentiate themselves from the next scooter company.

Okay - so locking down scooter OEMs is a good thing for Gogoro and will help grow their business! The revenue projections aren’t entirely smoke - per the fine folks at McKinsey.

Gogoro, ultimately, is very much a traditional hardware company. The SaaS-like recurring revenue features of the company make for good headlines but don’t appear to be the big business drivers for the company (yet). However, they’ve done great things expanding in Taiwan and I can’t wait for their growth in the more mature and more demanding China and India markets!

The Ultimate Question:

Having thought about Gogoro for so long, the ultimate bonus question for me to contend with is - will I buy the Gogoro stock, or recommend that my friends do?

There’s only so much you can tell from a window-dressed S-1 deck. The numbers, as I see it, are just fine. Not bad, not great. Execution wise - no one else is doing it at the scale they are.

For me personally, the allure is more than just financial. I do believe in Gogoro’s story and their vision for electrifying large two-wheeler fleets. I think back to many hours stuck in Delhi traffic with no option but to breathe in fumes from the countless scooters and motorcycles around me. With Gogoro, I envision the sputtering of ICE scooters being replaced with quiet, whirring motors. Far less noxious fumes to go around. Gogoro won’t make Delhi’s traffic jams go away, but they’ll make it bearable (and breathable!) to be stuck in one.

Yeah, I think I will recommend the stock to friends. As kids these days say - YOLO.

Bonus Content:

That’s all from me folks. Have a great week!

👇 Please hit the ❤️ button below if you enjoyed this post. Or leave a comment!

Good summary of the tech. However there is a big error in your "Pack cost over its lifetime" calculation.

You assume 365 cycles per year, which is one per day. The $29USD per month plan gives 630km of range. 630km would be just over 4 battery swaps per month with the 150-170km range on a 2 battery scooter. Or 1 swap per week, rather than 1 per day.

If someone drives the full 150-170km per day they will need to pay for a more expensive plan.

Diving recharging cost by 7 reduces the pack cost over lifetime from $1098 to $404.

It should also be noted that this is a $29USD per month 2 battery plan. Which means $174 of yearly revenue per battery, rather than the $124 calculated (which must assume most users having cheaper plans).

This increases the pack revenue for this usage rate from $1240 to $1740.

With these numbers lifetime profit should be closer to $1336 than $142.

However, I think your estimate for pack cost is a bit generous. So I'd estimate ~$1000.